Tags: BNSF / Risk / Earnings

This fanpage is not officially affiliated with Berkshire Hathaway: Disclaimer

When the Smoot-Hawley Tariff Act of 1930 helped transform a stock market crash into the Great Depression, America's railroads watched their freight volumes collapse by over 50% in three years. Nearly a century later, BNSF Railway — Berkshire Hathaway's $34.5 billion crown jewel of infrastructure — finds itself once again on the front line of a trade war, this time with tariff rates that make Smoot-Hawley look restrained. At 145% on Chinese goods at their April 2025 peak, the current levies are not merely protectionist signals; they are economic blockades. For a railroad that derives its largest revenue segment from containers arriving at West Coast ports and ships grain to Asia through Pacific Northwest terminals, the implications are profound — and different from every other Class I railroad in North America. ↗

Introduction

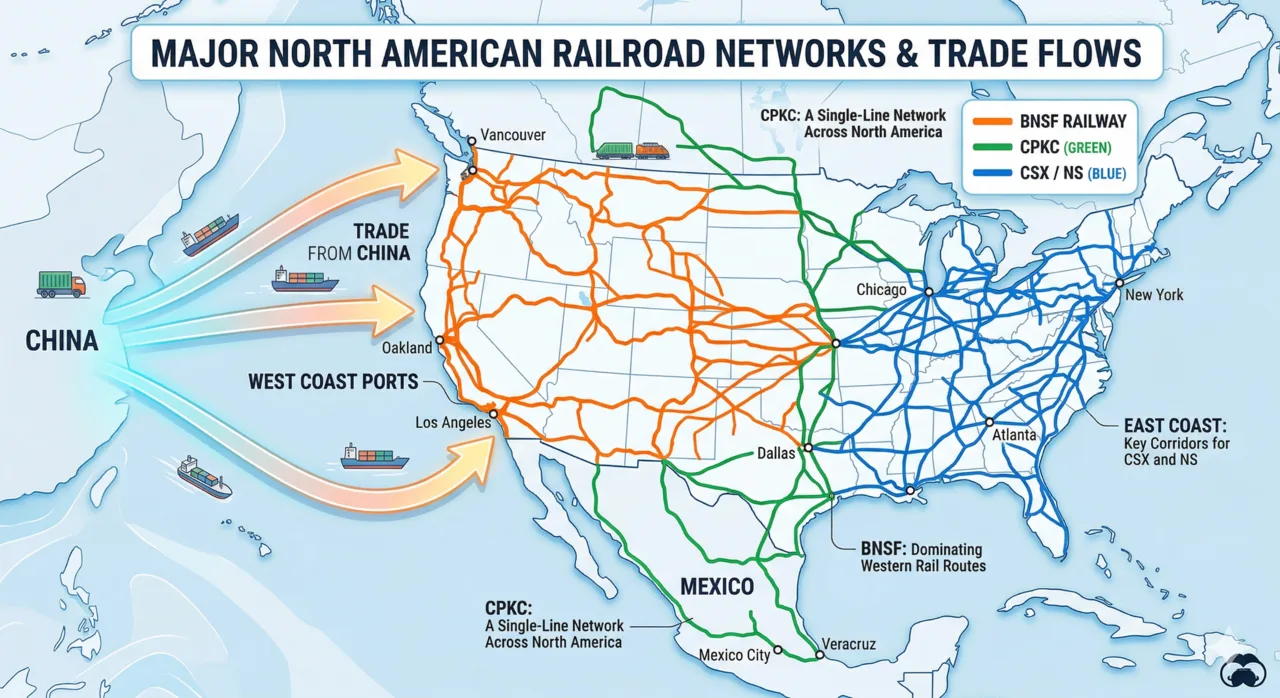

BNSF Railway operates over 32,500 route miles of track across 28 states, employs approximately 35,000 people, and generated $23.4 billion in revenue in 2025 1. It is, by any measure, a colossus. But it is a colossus with a very specific geographic orientation: westward, toward the Pacific. BNSF and Union Pacific are the only two railroads with on-dock rail access at the Ports of Los Angeles and Long Beach — the gateway through which roughly one-third of all U.S. container imports pass 2. In 2025, BNSF set a new annual record at those ports with 1,615,156 on-dock container lifts, surpassing its own 2024 record by more than 125,000 units 3.

This Pacific orientation is a tremendous asset in normal times. In a trade war with China, it becomes a liability. The Association of American Railroads estimates that international trade directly drives 37-38% of total U.S. rail traffic and revenue 4. For BNSF, that exposure skews even higher because of its West Coast intermodal dominance and its role as a primary conduit for agricultural exports bound for Asia.

Meanwhile, BNSF's Mexico freight volume accounts for just 3.8% of its total traffic 1 — a fraction of what Union Pacific or CPKC handle. In a world where nearshoring to Mexico is the most obvious tariff hedge, BNSF has the smallest escape valve among its peers.

The Pacific Gateway Under Siege

BNSF's Consumer Products segment — which includes intermodal containers, automotive, and other consumer goods — is the railroad's largest by volume at 5,601 thousand cars in 2025 1. The annual report explicitly credits "higher intermodal shipments resulting from higher West Coast imports" as the primary volume driver in both 2024 and 2025 1. When containers flow through Long Beach and Los Angeles, BNSF prospers. When they don't, BNSF feels it first and hardest.

The tariff saga of 2025 played out in three brutal acts.

Act One — the frontloading surge. From January through March, U.S. importers raced to stockpile goods ahead of anticipated tariff hikes. BNSF's Q1 Consumer Products volumes surged 9% year-over-year 5. The Port of Los Angeles processed record volumes, and warehouses across Southern California filled to capacity. It was the import equivalent of a bank run — everyone rushing to get goods through the door before it slammed shut.

Act Two — Liberation Day. On April 2, 2025, tariffs on Chinese goods spiked to 145%. The effect was immediate and savage. The Port of Los Angeles projected a 35% drop in vessel arrivals by early May 6. Hapag-Lloyd reported China-to-U.S. container bookings plunged roughly 30%, with some weeks seeing cancellation rates even higher 7. On the rail side, eastbound international container volume on BNSF and UP main lines in Southern California sank to its lowest level in six months during the week of May 19 — down 26.3% from the March peak 8. Port of Los Angeles Executive Director Gene Seroka noted that approximately 40% of the port's import business was tied to China 6, down from 60% at the start of the first trade war in 2018, but still an enormous concentration.

Act Three — the truce and the hangover. The 90-day U.S.-China tariff truce announced May 12 dropped rates to 30%, triggering an immediate container rebound. Hapag-Lloyd saw a 50% week-over-week surge in China-U.S. bookings 7. BNSF had prepared: Jon Gabriel, the railroad's Group VP of Intermodal, had staged over 100 locomotives in a "surge fleet" in California alone — some nine miles of locomotives lined up — plus 8,000 additional intermodal parking spaces across the network 9. But the truce could not undo the damage already baked in. Q4 2025 Consumer Products volumes fell 6%, and for full-year 2025 the segment managed just 1% growth — a stark deceleration from 2024's 16% surge 10.

| Period | Consumer Products Volume Change | Key Driver |

|---|---|---|

| Full Year 2024 | +16.2% | West Coast import surge, new intermodal customer1 |

| Q1 2025 | +9% | Tariff frontloading5 |

| Q4 2025 | -6% | Post-tariff demand destruction10 |

| Full Year 2025 | +1% | Frontloading gains offset by H2 decline10 |

| First 10 weeks 2026 | ~-8% vs. prior year | Ongoing trade uncertainty11 |

The pattern heading into 2026 is ominous. North American intermodal volumes through the first ten weeks of the year are running nearly 8% below 2025's pace 11. The whiplash between frontloading, collapse, truce-driven recovery, and renewed uncertainty has made planning nearly impossible for shippers and railroads alike.

Grain Under Fire

If intermodal is BNSF's most visible tariff wound, agriculture may be the deeper one. BNSF hauls enormous volumes of grain from the Northern Plains to Pacific Northwest export terminals — a primary artery for U.S. agricultural products bound for Asia. When China imposed retaliatory tariffs in March 2025 — 10% on soybeans and sorghum, 15% on wheat, corn, and cotton — it targeted approximately $21 billion in U.S. agricultural exports 12. Soybeans alone accounted for $12.8 billion of that figure 12.

The consequences were unprecedented. For five consecutive months in 2025, zero U.S. soybeans were exported to China — a drought in trade that had not occurred in three decades of modern commerce between the two nations 13. U.S. soybean exports to China totaled roughly 218 million bushels for the year, down from nearly one billion bushels the prior year 13. China simply pivoted to Brazilian suppliers, importing record volumes between April and July. Soybean prices dropped 12-15% compared to April 2024 levels 12.

Matt White, BNSF's assistant VP of agricultural products marketing, described the operational pivot: "Without demand for soybean exports out of the PNW, the market needed to pivot on where soybeans needed to be shipped" 13. BNSF redirected soybean shuttle trains south to Gulf ports in September and October — a logistical adjustment, but not an economic one. Gulf port routes are longer, more congested, and ultimately less profitable per unit than the direct Pacific Northwest-to-Asia corridor.

Yet the grain story was not uniformly dark. BNSF's corn volumes hit an all-time annual record in 2025 — the highest since 2018 13. Oil seeds and meals reached record volumes. Ethanol shipments set an all-time mark 13. The Agricultural and Energy Products segment ended 2025 up 2% in volume and 3.2% in revenue 1. Diversification within the grain franchise partially offset the China soybean loss, but the structural risk remains: if retaliatory tariffs persist, BNSF's most direct export corridor — the Pacific Northwest — loses its raison d'etre for an entire commodity class.

Industrial Collateral Damage

BNSF's Industrial Products segment was the clearest tariff casualty in the 2025 financials. Full-year volumes declined 5%, with Q4 showing a 7% drop 10. The culprits were lower shipments of construction products, plastics, and petroleum products 1.

The mechanism is indirect but powerful. Section 232 tariffs pushed steel and aluminum duties to 25-50%, adding an estimated $22.4 billion in costs to U.S. steel and aluminum imports 14. Those costs ripple downstream into construction, manufacturing, and infrastructure projects — all of which generate carload freight for BNSF. When a developer shelves a project because steel costs jumped 30%, BNSF loses the aggregates, the lumber, the machinery, and the finished materials that would have moved by rail. ↗

This creates an ironic tension within Berkshire's own portfolio. BNSF's 2025 annual report highlights $5.3 billion in customer investments at rail-served facilities — 117 projects creating over 1,200 jobs 1. The railroad's long-term thesis depends on industrial expansion along its corridors. Tariff-induced uncertainty freezes exactly that kind of capital deployment.

The 2019 Playbook — at Six Times the Rate

The 2018-2019 trade war provides a direct historical precedent for what BNSF faces — and a sobering one, given that 2025's tariffs peaked at 145% versus 25% in 2019.

During the first trade war, BNSF's Consumer Products revenue slipped 0.5% for full-year 2019 on volume decreases of 4.6% 15. Agricultural Products volumes fell 5% due to "export competition from non-U.S. sources and the impact of international trade policies" 15. The Intermodal Association of North America called 2019 "a very challenging year for the North American intermodal industry" — the worst since the 2009 recession 16.

The broader damage was structural. U.S. intermodal compound annual growth shifted from +2.5% during 2014-2018 to -1.7% during 2018-2023 16 — a multi-year drag that persisted well beyond the tariffs themselves. In June 2019, the Port of Los Angeles Executive Director wrote directly to U.S. Trade Representative Robert Lighthizer, noting that current and proposed tariffs would impact 64% of container volume at the ports of LA and Long Beach, explicitly identifying BNSF and UP as downstream victims 16.

The 2025 situation is structurally identical but larger in every dimension. The tariff rates are nearly six times higher. The volume swings are sharper. The retaliation is broader. And unlike 2019, when the trade war was essentially bilateral, the 2025 "Liberation Day" tariffs initially targeted dozens of nations before being partially walked back.

If the 2019 precedent holds at amplified scale, BNSF shareholders should expect not merely a quarter or two of softness, but a multi-year intermodal growth headwind that outlasts the tariffs themselves — as supply chains, once redirected, do not snap back overnight.

The Competitor Gap

Not all railroads are created equal in a trade war, and the asymmetry of exposure across Class I carriers tells a revealing story.

| Railroad | Primary Exposure | Mexico Volume Share | Key Tariff Risk |

|---|---|---|---|

| BNSF | West Coast / Pacific intermodal | ~3.8%1 | Highest: China container imports + grain exports |

| Union Pacific | West Coast / Pacific + Mexico | ~11%17 | High: similar intermodal, but Mexico offsets |

| CSX | Atlantic / Gulf Coast ports | Low17 | Moderate: less Pacific, more diversified |

| Norfolk Southern | Eastern / Atlantic | Low17 | Moderate: may gain from East Coast port diversion |

| CPKC | Canada-Mexico corridor | High17 | Lowest: USMCA partners exempt from reciprocal tariffs |

The contrast with CPKC is particularly striking. When the April 2 tariff announcement landed, CPKC's stock dropped just 0.7%, while UP fell roughly 6% and Norfolk Southern nearly 5% 17. Analyst Bascome Majors of Susquehanna Financial Group captured the dynamic precisely: the tariff announcements were "less onerous than feared for North American trade partners Canada and Mexico and worse than feared for China and other U.S. trade partners in Asia" 17. BNSF, as the most Asia-Pacific-oriented of all Class I railroads, sits on the wrong side of that equation.

Union Pacific shares BNSF's West Coast intermodal exposure but has a critical hedge: Mexico accounts for roughly 11% of UP's revenue 17. As nearshoring accelerates — Mexico absorbed $41 billion in foreign direct investment in the first three quarters of 2025, a 15% year-over-year increase 18 — UP and especially CPKC stand to capture the redirected freight. BNSF's 3.8% Mexico share offers almost no buffer. Its 2025 launch of the "Quantum de Mexico" service with J.B. Hunt and GMXT signals awareness of the gap, but it remains a marginal contributor 3.

Eastern railroads like CSX and Norfolk Southern face an even more favorable calculus. When trans-Pacific tariffs drive importers to reroute through East Coast and Gulf ports — shortening supply chains and avoiding West Coast congestion — the traffic literally shifts toward CSX and NS networks and away from BNSF and UP. The "double whammy" analysts warn of — lower total imports plus a lower West Coast share — applies only to the western carriers 17.

Abel's Margin Dilemma

Greg Abel, who became Berkshire Hathaway's CEO at the end of 2025, has been unusually direct about BNSF's operating performance gap. In his shareholder letter, Abel noted that BNSF's operating margin improved to 34.5% in 2025 from 32.0% in 2024, but added bluntly: "The gap to the industry's best remains too wide and closing it will require continued improvements in efficiency and service" 1. ↗

The math Abel laid out is stark: each one-percentage-point improvement in operating margin generates approximately $230 million in incremental operating cash flow 1. Union Pacific's 2025 operating ratio was approximately 59.8% — an operating margin of 40.2% compared to BNSF's 34.5% 19. That 5.7-percentage-point gap represents roughly $1.3 billion in annual cash flow that BNSF is leaving on the table.

The tariff environment works directly against Abel's margin improvement goal. Operating margin expands through either revenue growth (spreading fixed costs over more volume) or cost reduction. A tariff-driven volume decline pressures both levers: fewer containers mean less revenue to absorb BNSF's substantial fixed-cost base of track maintenance, locomotives, and labor, while the unpredictable surge-and-collapse pattern of trade policy makes it nearly impossible to right-size the workforce or asset base.

BNSF generated $8.1 billion in net operating cash flows in 2025 and returned $4.4 billion to Berkshire through dividends 1. The dividend has averaged $4.1 billion annually over the past five years 1. These are impressive numbers, but they underscore the stakes: a sustained trade-driven volume decline of even 5-10% would meaningfully erode the cash flow that has made BNSF one of Berkshire's most reliable dividend machines. BNSF also carries $24.1 billion in standalone debt — not guaranteed by Berkshire — making its own cash generation essential for debt service 1.

At his final annual meeting in May 2025, Warren Buffett offered his most pointed commentary on the trade war: "Trade should not be a weapon," he said. Tariffs "can be an act of war" and "I think it's led to bad things" 20. For a man who spent $34.5 billion on a railroad whose prosperity is intertwined with global commerce, the comment was not merely philosophical — it was financial.

The Long Bet

Despite the headwinds, BNSF is not retreating from its Pacific orientation. If anything, it is doubling down.

The $1.5 billion Barstow International Gateway — a 4,500-acre facility that would be the largest intermodal terminal in North America, twice the size of the current largest — remains on track for construction beginning in late 2026 21. The project is designed to reduce container dwell time at LA and Long Beach by enabling faster transloading from international to domestic containers further inland. It is, fundamentally, a multi-decade bet that trans-Pacific trade will not only survive the current tariff regime but grow beyond it. ↗

BNSF is also aggressively pursuing domestic intermodal conversion. Chief Marketing Officer Tom Williams estimated that 7-11 million additional truckload shipments could potentially shift from highway to rail 22. With the trucking market mired in excess capacity and BNSF achieving historically low terminal dwell times throughout 2025 3, the conditions for truck-to-rail conversion are favorable. New service products launched in 2025 — LA-to-Houston third-day service, Pacific Northwest-to-Chicago six-day service (the fastest from any PNW gateway), and a coast-to-coast intermodal partnership with CSX connecting Southern California to Charlotte, Jacksonville, and Atlanta 23 — all target domestic freight that is immune to tariff disruption.

Intermodal analyst Larry Gross, who has been among the most bearish voices on the 2025-2026 trade outlook, conceded he was "a little bit optimistic with regard to the share gain" from domestic intermodal growth 11. The logic is compelling: if international intermodal volumes contract, the truck-to-rail conversion pipeline becomes not just a growth opportunity but an existential necessity for maintaining network utilization.

BNSF's total 2026 capital plan stands at $3.6 billion, including $358 million for expansion and efficiency projects 24. The railroad is spending as if the future of Pacific trade is bright, even as the present is clouded.

Conclusion

BNSF Railway enters 2026 in an uncomfortable position for a Berkshire Hathaway subsidiary: it is the best-in-class operator of a franchise whose core value proposition — moving goods between Asia and America's interior — is under direct political assault. The numbers tell a story of a railroad whipsawed by policy: frontloading surges followed by volume collapses, soybean exports zeroing out while corn hits records, intermodal parking spaces added by the thousands for containers that may or may not arrive.

The risks are real and specific. International trade drives 37-38% of U.S. rail revenue 4. BNSF's West Coast orientation concentrates that exposure. Its tiny Mexico footprint limits its nearshoring hedge. The 2019 precedent suggests volume headwinds that outlast the tariffs themselves. And Abel's operating margin improvement campaign — worth $230 million per percentage point — runs directly into the wall of tariff-induced volume uncertainty.

But BNSF is not a passive victim. The Barstow bet, the domestic intermodal conversion push, the CSX coast-to-coast partnership, and the grain franchise's proven ability to pivot between export corridors all speak to operational resilience. BNSF has survived worse: the Great Depression, the postwar highway boom, deregulation, and the slow death of coal. Each time, the railroad adapted — sometimes over years, sometimes over decades.

The question for Berkshire shareholders is not whether BNSF will survive the trade war. It will. The question is whether it can close the gap to Union Pacific's margins while simultaneously absorbing the most concentrated tariff impact of any North American railroad. Abel has staked his credibility on that promise. The tariffs are testing it.

References

-

Berkshire Hathaway 2025 Annual Report - berkshirehathaway.com ↩↩↩↩↩↩↩↩↩↩↩↩

-

BNSF sets new container volume record at Southern California ports - trains.com ↩

-

BNSF 2025 in review - bnsf.com ↩↩↩

-

AAR sees 'uncertainty' for US railroads in 2025 - freightwaves.com ↩↩

-

BNSF boosts revenue, income in Q1 - progressiverailroading.com ↩

-

Port of Los Angeles says shipping volume will plummet 35% - cnbc.com ↩↩

-

Hapag-Lloyd saw China bookings drop hard after US enacted tariffs - joc.com ↩↩

-

Southern California international intermodal volume sees weekly decline - freightwaves.com ↩

-

This railroad has 100 extra locomotives ready to handle a container surge - freightwaves.com ↩

-

BNSF reports net income gains in Q4, full-year 2025 - progressiverailroading.com ↩↩

-

TD Cowen 1Q26 Rail Preview: Quarterly Rail Survey - railwayage.com ↩↩

-

US Tariffs on Steel and Aluminum: Analyzing Impacts - bcg.com ↩

-

BNSF posts revenue decline on lower volumes in Q4, full-year 2019 - progressiverailroading.com ↩↩

-

IANA's Market Trends Report: low intermodal volumes for 2019 - logisticsmgmt.com ↩↩↩

-

New US tariffs hit railroad stocks in early trading - freightwaves.com ↩↩↩↩

-

Nearshoring Manufacturing in Mexico Will Keep Thriving in 2025 - novalinkmx.com ↩

-

BNSF's margin gap vs Union Pacific - blog.gettransport.com ↩

-

Warren Buffett knocks tariffs: 'Trade should not be a weapon' - cnbc.com ↩

-

BNSF's trade-related intermodal projects move ahead despite tariffs - freightwaves.com ↩

-

For BNSF, 2025 Revenue, Volume Flat - railwayage.com ↩

-

CSX, BNSF announce new intermodal services - investors.csx.com ↩

-

BNSF plans $3.6 billion spending plan for 2026 - dcvelocity.com ↩