Tags: Fechheimer / Warren Buffett / Greg Abel

This fanpage is not officially affiliated with Berkshire Hathaway: Disclaimer

On January 15, 1985, Warren Buffett opened a letter from a man he had never heard of, about a company he did not know existed. The writer was Bob Heldman of Cincinnati, a Berkshire shareholder of long standing and chairman of a uniform manufacturer called Fechheimer Brothers. He thought his business met Buffett's tests and suggested they talk.1 Sixteen months later — on June 3, 1986 — Berkshire owned 84% of it, and Buffett had still never set foot in Cincinnati.4 Forty years on, that letter is worth revisiting, not for nostalgia, but because it describes an acquisition Berkshire is now too large to make — and because Greg Abel, in his very first letter as chief executive, just proved the instinct behind it is still alive.

The letter from a stranger

Fechheimer had been making uniforms since 1842 — for police, fire departments, the postal service, transit workers, and the military.2 Bob Heldman's father Warren had joined the family firm in 1941; Bob and his brother George, the president, ran it alongside their sons. In 1981 the family had sold to a group of venture capitalists in a leveraged buyout while keeping an equity stake; by 1985 the debt was paid down, the venture investors wanted out, and Bob — "having dutifully read Berkshire's annual reports," as Buffett put it — thought of Omaha.1 Berkshire bought roughly 84% of the stock at a price based on a $55 million valuation for the whole business, with the Heldmans retaining the rest.3

What makes the deal a template rather than an anecdote is how Buffett bought it. He did no plant tour, commissioned no consultants, kicked no tires. He said so in the 1986 letter, with obvious relish:

"You may be amused to know that neither Charlie nor I have been to Cincinnati, headquarters for Fechheimer, to see their operation… If our success were to depend upon insights we developed through plant inspections, Berkshire would be in big trouble."4

This was not laziness; it was doctrine. Buffett was buying a management team and a set of economics he could read off the numbers, and he explicitly likened the transaction to his purchase of the Nebraska Furniture Mart — most of the shares held by people who wanted to redeploy their capital, a family who loved the work and wanted to keep running and owning it. "Both Fechheimer and NFM were right for us, and we were right for them," he wrote.6 Three years later he would describe his role as owner in one of his best throwaway lines: "We're much like the lonesome Maytag repairman: The Heldman managerial product is so good that a service call is never needed."8

Fechheimer did not arrive alone. The very same year, Berkshire closed the Scott Fetzer acquisition ↗ — a $320 million Cleveland conglomerate that Buffett had also chased with a cold letter, this one to CEO Ralph Schey, "whom I did not know," after a rival buyout collapsed.7 Two companies, one small and one large, both landing in 1986, both sourced not through investment bankers but through the mail. If you want a single year in which the letter-and-trust acquisition method was proven out, it is this one. And the reciprocity Buffett prized ran both ways: as he liked to note, Chuck Huggins had run See's Candies ↗ for fifteen years without ever visiting Omaha.

The prototype with one flaw

Buffett clearly adored the Fechheimer deal — as the biographer Alice Schroeder observed, what "still made his pulse race was buying a company like Fechheimer, which made prison-guard uniforms."27 But even in the 1986 letter, at the very moment of celebrating it, he named the one thing wrong with it:

"As a prototype for acquisitions, Fechheimer has only one drawback: size. We hope our next acquisition is at least several times as large but a carbon copy in all other respects."9

Read that sentence again, because it is the hinge of this entire story. In 1986 the flaw was small and forgivable: Fechheimer used "only about 2% of Berkshire's net worth," and Berkshire's net worth that year was about $2.4 billion.5 A $55 million deal was a rounding error even then — but a tolerable one, because Berkshire itself was small enough that a stream of $13-million-a-year pre-tax earnings still mattered at the margin. Fechheimer joined the roster of businesses Buffett fondly nicknamed the "Sainted Seven," earned its keep quietly, and asked for nothing.

The problem is that the flaw Buffett flagged in 1986 did not stay small. It grew — compounding right alongside the businesses — until it swallowed the entire model.

The silence has a shape

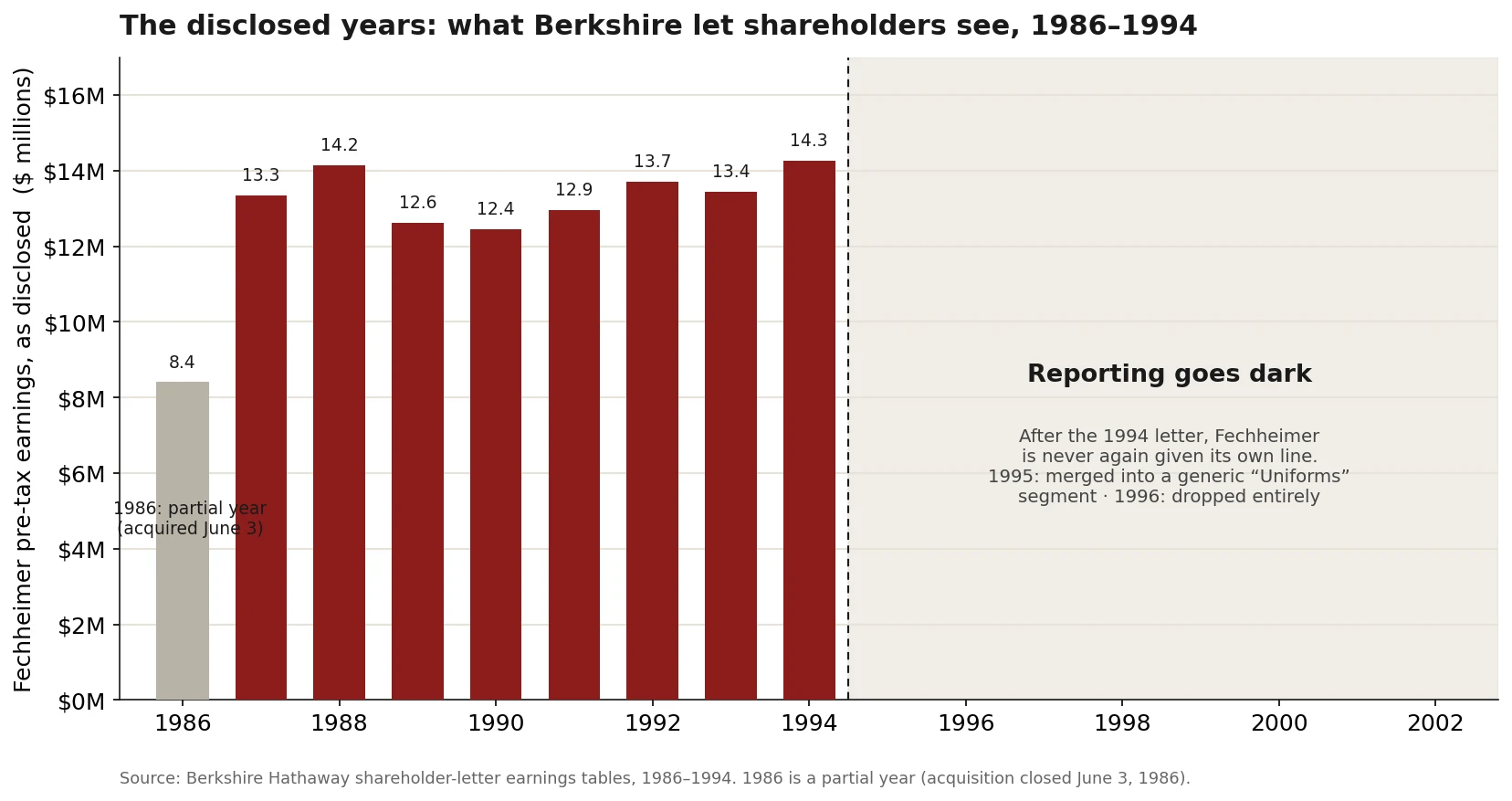

You can watch it happen in Berkshire's own disclosures. For nine years, from the 1986 letter through the 1994 letter, Fechheimer appeared as a named line in Berkshire's earnings tables, its pre-tax profit printed for all to see — $8.4 million in the partial first year, then settling into a comfortable $12–14 million band.10 Then the reporting went dark.

The 1994 letter was the last time Fechheimer's earnings were ever broken out.11 In the 1995 annual report the company vanished into a generic "Uniforms" segment — revenue $143.8 million, operating profit $16.1 million — no longer named in the table by its own initials.12 A year later that segment disappeared too, as Berkshire's growing bulk let it collapse seven reportable non-insurance segments into six.13 By 2002 the company confirmed in a footnote what had quietly become true years earlier: Fechheimer was "not part of a reportable segment," folded permanently into an anonymous "Apparel" grouping alongside Fruit of the Loom, Garan, and H.H. Brown.14

This is what "buy it, trust the managers, and go quiet" looks like when you plot it. The silence is not neglect — it is the visible signature of the method. A business too good to need a service call is also, eventually, too small to warrant a sentence.

| Era | How Fechheimer appeared in Berkshire's reporting | What a shareholder could see |

|---|---|---|

| 1986–1994 | Named line in the earnings table + periodic profile paragraphs | Annual pre-tax earnings10 |

| 1995 | Merged into a generic "Uniforms" segment | Segment revenue & operating profit12 |

| 1996–2001 | Dropped from segment reporting; name-only in subsidiary lists | Nothing but the name13 |

| 2002–present | Absorbed into the "Apparel" grouping | A one-line description + an employee count14 |

The last trace

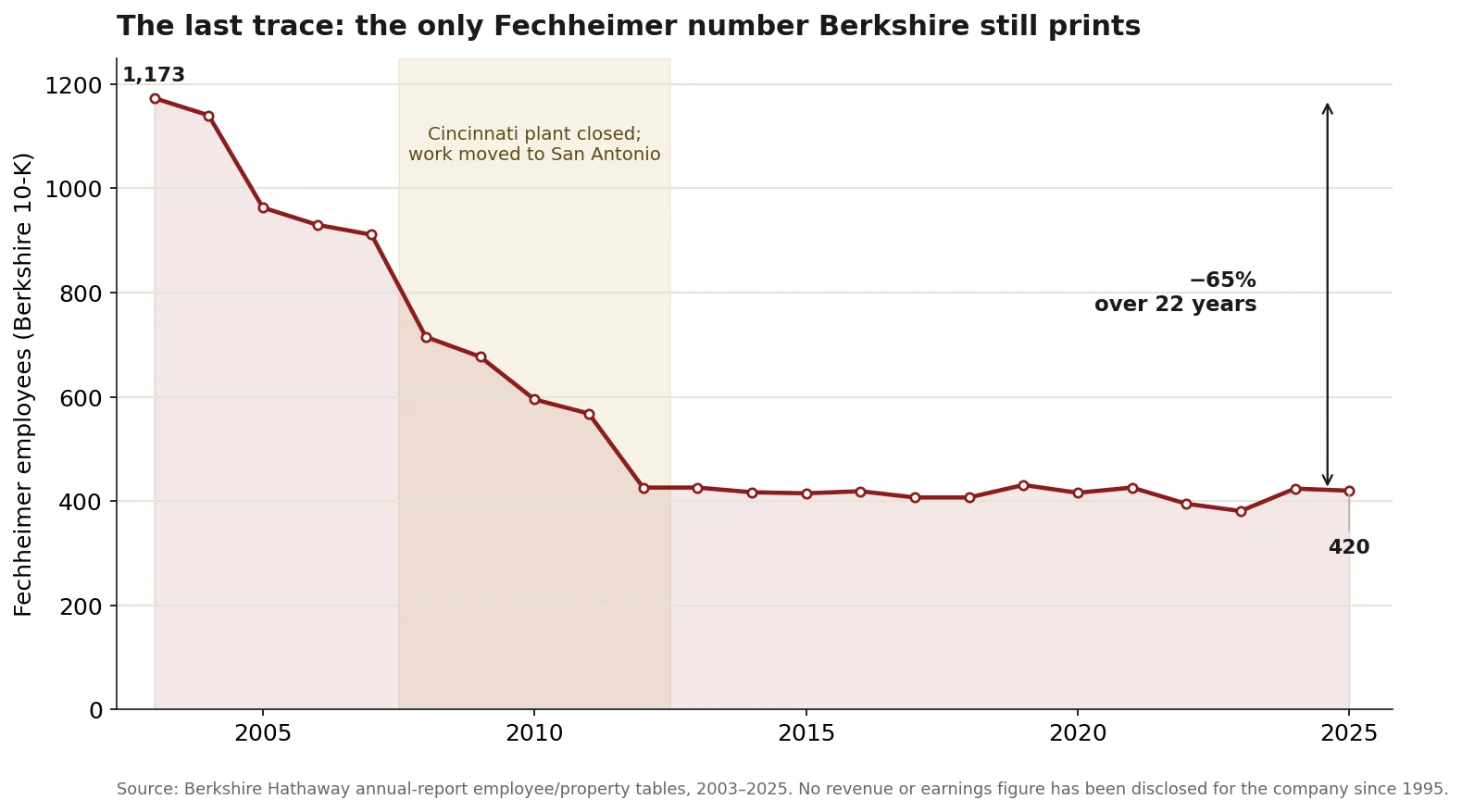

After 2001, Berkshire's filings disclose exactly one number about Fechheimer, and they still disclose it every year: how many people it employs. It is the last quantitative trace of the company in the public record — and it tells its own story.

The workforce fell from 1,173 in 2003 to 420 in 2025 — down roughly 65% in twenty-two years.15 The steepest drop coincides with a decision the annual reports never mention but the biographer Lawrence Cunningham recorded: Fechheimer "once closed its Cincinnati plant — where it had operated for more than a century — and moved to lower-cost San Antonio and ultimately shuttered that facility."16 A 182-year-old manufacturer became, in large part, a distributor and brand-holder. Today the company still operates out of Cincinnati under Berkshire's ownership, selling public-safety and tactical uniforms through brands like Flying Cross and Vertx.17 Its revenue is no longer disclosed by Berkshire and can only be estimated — an exercise worth doing carefully, and one that says as much about the limits of the public record as about the company.18

So was the acquisition a success? On the only evidence Berkshire ever provided, unambiguously yes. Across the nine years it disclosed, Fechheimer earned roughly $115 million in cumulative pre-tax profit — more than twice the $55 million Buffett valued the entire company at in 1986.28 In pre-tax terms the business paid for itself about twice over before the reporting even went dark, and in forty years of ownership it has never once surfaced on the list of Berkshire's write-downs or regrets — no small distinction in a portfolio that also holds the roughly $10.6 billion Precision Castparts impairment ↗ and the infamous Dexter Shoe wipeout. What it was not is a needle-mover: it never scaled, never compounded into something large, and today employs a third of the people it once did. That is precisely the point. Fechheimer succeeded in the specific, modest way small acquisitions are supposed to — cheap to buy, quick to self-fund, endlessly low-maintenance — which is exactly why Buffett filed it under "prototype" rather than "triumph."

None of this, then, is a decline story about Berkshire. It is a decline story about disclosure — and, underneath it, a business that has done exactly what Buffett bought it to do: run itself, throw off cash, and never need a service call. The point is what it reveals about scale. A company can go from headline acquisition to un-mentioned footnote without anything going wrong at all, simply because the parent around it grew a thousand-fold.

The deal Abel can no longer make

Which brings us to the flaw Buffett named in 1986, now grown monstrous. Berkshire's net worth at the end of the first quarter of 2026 was $727 billion, with roughly $397 billion sitting in cash and Treasury bills.19 Run the same ratio Buffett ran in 1986. A deal worth "about 2% of Berkshire's net worth" today would be a $14.5 billion acquisition — larger than all but a handful of transactions in the company's history. And an actual $55 million deal, the size of the original Fechheimer, would today amount to 0.0076% of net worth: not a rounding error but a rounding error's rounding error, too small for Berkshire's headquarters to notice, let alone staff, negotiate, and integrate.20 Buffett has said for years that "size is the enemy of performance," and nowhere is the enemy more visible than here.26 The letter-sourced small-family-business purchase — the deal Buffett called his prototype — is not a strategy Berkshire retired. It is one that arithmetic retired for it.

Watch what Abel's Berkshire actually buys and the size wall is obvious. His inheritance closed with the $9.7 billion OxyChem acquisition in January 2026, and his own first major deal as CEO was the roughly $6.8 billion agreement to buy the homebuilder Taylor Morrison ↗ in May 2026.2324 These are elephants, exactly as the 1986 letter hoped the "next acquisition" would be — "several times as large" than Fechheimer. What they cannot be is a "carbon copy in all other respects," because the thing that made Fechheimer a carbon copy — a founding family, a modest price, a business you could buy on trust from a letter — does not scale to $10 billion. The bigger the check, the more bankers, boards, and diligence stand between Omaha and the deal.

Bell Laboratories, or why the method survives

And yet. Turn to Greg Abel's first shareholder letter, attached to the 2025 annual report, and you find the Fechheimer story told again — forty years later, in almost the same words, by a different man.

In 2025 Berkshire acquired Bell Laboratories — no relation to the storied telecommunications research lab that gave us the transistor, but a family-owned maker of rodenticides in Windsor, Wisconsin — for an undisclosed sum.22 Here is how Abel described it:

"Last year, Warren received a letter from Steve Levy, Bell Laboratories' CEO, asking that we look at his business… Steve's letter was perfect. Bell Laboratories meets a persistent need: rodent control… durable advantages and long-term economic prospects run by excellent managers. We only wish it had been ten times bigger."21

Read it against the 1986 line — "we hope our next acquisition is at least several times as large but a carbon copy in all other respects" — and the rhyme is uncanny. A letter arrives, unsolicited, from the chief executive of a boring, durable, family-run niche manufacturer. Berkshire buys it on the strength of the numbers and the people. And the only regret, the only flaw, is the same one Buffett named the year of Fechheimer: it is too small. The method is not dead. It is a living inheritance — Abel chose to tell exactly this kind of story in his debut letter — but it now runs into the identical wall, only forty years higher.

So where does a genuinely Fechheimer-sized deal happen at today's Berkshire? Increasingly, not at headquarters at all, but one level down. Buffett described the migration himself back in 2013: "While Charlie and I search for elephants, our many subsidiaries are regularly making bolt-on acquisitions… Last year, we contracted for 25 of these… ranged from $1.9 million to $1.1 billion in size."25 The letter-sourced small-durable-business purchase survives — inside Marmon's roughly hundred businesses, inside the building-products cluster, inside the utilities — where a $55 million tuck-in is a rational use of a divisional manager's time. What died was not the model but the model at the parent level, where Abel now must swing an elephant gun or not fire at all.

What a uniform maker teaches

There is a case to be made that you learn more about how Berkshire actually works from Fechheimer than from any of its famous holdings. The Apples and Coca-Colas teach you what Buffett buys. Fechheimer teaches you what Berkshire is: a place where a great small business can be acquired on trust, handed back its own keys, quietly compounded for four decades, and never bothered — to the point that the parent stops mentioning it at all. The silence in the filings is not the sound of a mistake. It is the sound of the system working exactly as designed.

The forty-year arc also carries a warning Abel has clearly absorbed. The very feature that made Fechheimer perfect — its smallness — is the feature Berkshire's success has made impossible to indulge at scale. Every dollar of net worth Buffett compounded raised the floor on what a deal must be worth to matter, until the prototype priced itself out. Abel's task is to keep buying carbon copies of Fechheimer's character — durable, well-run, bought on trust — at ten, a hundred, a thousand times Fechheimer's size. His wish that Bell Laboratories "had been ten times bigger" is the whole job description in nine words. The letters still arrive in Omaha. The trick, now, is that the good ones have to be for much, much larger companies — and the small, perfect ones, the Fechheimers, have to be waved down the hall to a subsidiary that is still small enough to care.

Somewhere in Cincinnati, 420 people are still making uniforms for the people who police, fight fires, and deliver the mail. Berkshire has not written a sentence about their revenue in thirty years. That, more than any headline deal, is what owning a business the Buffett way finally looks like. It began with a letter, much like the family enterprises ↗ Berkshire has quietly kept running for generations — and it is still, forty years later, quietly running.

References

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — “On January 15th of last year I received a letter from Bob Heldman of Cincinnati, a shareholder for many years and also Chairman of Fechheimer Bros. Until I read the letter, however, I did not know of either Bob or Fechheimer.” ↩↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — “Fechheimer, a uniform manufacturing and distribution business, began operations in 1842.” Warren Heldman joined in 1941; sons Bob and George (then president) and their sons subsequently joined. ↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — “we quickly purchased about 84% of the stock for a price that was based upon a $55 million valuation for the entire business.” (The Heldman family retained ~16%.) ↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — “neither Charlie nor I have been to Cincinnati, headquarters for Fechheimer, to see their operation… If our success were to depend upon insights we developed through plant inspections, Berkshire would be in big trouble.” ↩↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — Fechheimer described as “utilizing only about 2% of Berkshire's net worth”; the letter's opening reports a 1986 gain in net worth of $492.5 million (26.1%), implying year-end net worth of roughly $2.4 billion. ↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — The acquisition circumstances are likened to the Nebraska Furniture Mart purchase: “Both Fechheimer and NFM were right for us, and we were right for them.” ↩

-

Warren Buffett, 1985 Letter to Shareholders - berkshirehathaway.com — Scott Fetzer acquired for about $320 million (plus ~$90 million pre-existing debt). Buffett on sourcing it: “I wrote a short letter to Ralph, whom I did not know… Charlie and I met Ralph for dinner in Chicago on October 22 and signed an acquisition contract the following week.” ↩

-

Warren Buffett, 1989 Letter to Shareholders - berkshirehathaway.com — “Though we purchased Fechheimer four years ago, Charlie and I have never visited any of its plants or the home office in Cincinnati. We're much like the lonesome Maytag repairman: The Heldman managerial product is so good that a service call is never needed.” ↩

-

Warren Buffett, 1986 Letter to Shareholders - berkshirehathaway.com — “As a prototype for acquisitions, Fechheimer has only one drawback: size. We hope our next acquisition is at least several times as large but a carbon copy in all other respects.” ↩

-

Warren Buffett, Letters to Shareholders 1986–1994 (segment earnings tables) - berkshirehathaway.com — Fechheimer pre-tax earnings by year ($M): 1986 8.4 (partial year, acquired 6/3/86); 1987 13.3; 1988 14.2; 1989 12.6; 1990 12.5; 1991 12.9; 1992 13.7; 1993 13.4; 1994 14.3. ↩

-

Warren Buffett, 1994 Letter to Shareholders - berkshirehathaway.com — Final year Fechheimer appears as a separately named line in Berkshire's earnings table ($14.26M pre-tax). ↩

-

Berkshire Hathaway 1995 Annual Report — segment data - berkshirehathaway.com — Fechheimer reported within a generic "Uniforms" segment: 1995 revenue $143.8M (down $7.4M / 4.9% from 1994), operating profit $16.1M. This is the last year Berkshire disclosed any revenue or profit figure attributable to the company. ↩

-

Berkshire Hathaway 1996 Annual Report — segment data - berkshirehathaway.com — The non-insurance segment count falls from seven to six as Berkshire's growing scale reduces the number of individually reportable businesses; the "Uniforms" segment ceases to be broken out. ↩

-

Berkshire Hathaway 2002 Annual Report - berkshirehathaway.com — “several other businesses that have been owned by Berkshire for many years but were previously not part of a reportable segment (H.H. Brown Shoe Group and Fechheimer).” Fechheimer is thereafter folded into the "Apparel" grouping with Fruit of the Loom and Garan. ↩

-

Berkshire Hathaway Annual Reports 2003–2025 — employee/property tables - berkshirehathaway.com — Fechheimer employee count: 1,173 (2003); 963 (2005); 715 (2008); 595 (2010); 426 (2012); 407 (2017); 395 (2022); 420 (2025). A decline of ~65% over 2003–2025. The employee count is the only Fechheimer-specific figure Berkshire has disclosed since 1995. ↩

-

Lawrence A. Cunningham, Berkshire Beyond Buffett: The Enduring Value of Values (Columbia University Press, 2014) - cup.columbia.edu — “Fechheimer once closed its Cincinnati plant — where it had operated for more than a century — and moved to lower-cost San Antonio and ultimately shuttered that facility.” Cunningham also records the deal terms (84% for ~$46 million, family retaining the rest) and that no party conducted a site visit or reciprocal due diligence. ↩

-

Berkshire Hathaway 2025 Annual Report — business description - berkshirehathaway.com — “Fechheimer Brothers Company ('Fechheimers') manufactures and distributes uniforms, principally for the public service and safety markets, including police, fire, postal and military markets.” Present-day consumer brands include Flying Cross (dress/duty) and Vertx (tactical); the company remains headquartered in Cincinnati, Ohio. ↩

-

How the revenue estimate is built — and why it is only an estimate. Berkshire has not disclosed any revenue figure for Fechheimer since fiscal 1995, when the "Uniforms" segment reported $143.8 million.12 After 1996 the company was dropped from segment reporting and, from 2002, absorbed into an "Apparel" grouping whose combined results are themselves no longer separately reported — so no top-down figure can be extracted from Berkshire's filings. The only official Fechheimer-specific number Berkshire still prints is its employee count (420 in 2025).15 Third-party data aggregators (e.g., IncFact, ZoomInfo) model current revenue at roughly $175–180 million, but these are estimates, not audited disclosures, and their own headcount figures (~140–190) conflict with Berkshire's 10-K figure of 420 — so the revenue number should be read as directional scale only, not a precise figure. For perspective, ~$178 million three decades after the last official $143.8 million (1995) implies only ~0.8% nominal annual growth — roughly flat in real terms — which is consistent with the ~65% workforce decline and a mature niche manufacturer that shifted from making to distributing. We therefore cite it as an outside estimate, not a Berkshire-reported result. Aggregator sources: IncFact — Fechheimer Brothers; ZoomInfo — Fechheimer Brothers. ↩

-

Berkshire Hathaway Q1 2026 Form 10-Q — Consolidated Balance Sheet - berkshirehathaway.com — Total Berkshire shareholders' equity $727,181 million at March 31, 2026. Cash, cash equivalents and short-term U.S. Treasury Bills totaled roughly $397 billion ($51,478M cash + $339,261M T-bills in Insurance & Other, plus $6,644M railroad/utilities/energy cash). ↩

-

Author's calculation. 2% of $727.2B net worth = $14.54B. A $55M deal ÷ $727.2B net worth = 0.00756%. 1986 comparison: Fechheimer's $55M ÷ ~$2.4B year-end 1986 net worth ≈ 2.3%, consistent with Buffett's "about 2%" description.5 Figures illustrate relative scale, not a specific deal. ↩

-

Greg Abel, 2025 Letter to Shareholders (in the 2025 Annual Report) - berkshirehathaway.com — “Last year, Warren received a letter from Steve Levy, Bell Laboratories' CEO, asking that we look at his business… The letter was perfect. Bell Laboratories meets a persistent need: rodent control… run by excellent managers. We only wish it had been ten times bigger.” (Abel wrote the 2025 letter, published early 2026 — his first as CEO.) ↩

-

Berkshire Hathaway 2025 Annual Report — subsequent/acquisition notes - berkshirehathaway.com — “Berkshire acquired Bell Laboratories, LLC ('Bell Laboratories') on July 31, 2025. Bell Laboratories produces high quality rodenticides and other rodent control products… and is headquartered in Windsor, Wisconsin.” ↩

-

Berkshire completes $9.7B acquisition of OxyChem - manufacturingdive.com — Berkshire completed the $9.7 billion purchase of Occidental Petroleum's chemicals business (OxyChem) on January 2, 2026; corroborated in the Berkshire 2025 Annual Report. ↩

-

Berkshire to acquire Taylor Morrison - cnbc.com — Announced May 31 / June 1, 2026: Berkshire agreed to acquire homebuilder Taylor Morrison for $72.50/share (~$6.8B equity, ~$8.5B including debt), a 24% premium — Greg Abel's first major acquisition as CEO. See also our piece The Whole Staircase. ↩

-

Warren Buffett, 2013 Letter to Shareholders - berkshirehathaway.com — “While Charlie and I search for elephants, our many subsidiaries are regularly making bolt-on acquisitions… Last year, we contracted for 25 of these, scheduled to cost $3.1 billion in aggregate. These transactions ranged from $1.9 million to $1.1 billion in size.” ↩

-

2016 Berkshire Hathaway Annual Meeting - buffett.cnbc.com — Buffett: “Size is the enemy of performance… to a significant degree.” A recurring theme across multiple annual meetings and letters as Berkshire's capital base grew. ↩

-

Alice Schroeder, The Snowball: Warren Buffett and the Business of Life (2008) - simonandschuster.com — “What still made his pulse race was buying a company like Fechheimer, which made prison-guard uniforms.” ↩

-

Author's calculation from the disclosed pre-tax earnings series.10 Summing Fechheimer's reported pre-tax earnings 1986–1994 ($M): 8.4 + 13.3 + 14.2 + 12.6 + 12.5 + 12.9 + 13.7 + 13.4 + 14.3 = $115.3M, set against the $55M valuation Buffett placed on the whole business at acquisition.3 The earnings figures are for the entire company (Berkshire owned ~84%) and are pre-tax; the comparison illustrates the deal's early cash-on-cost, not a full-period return, since Berkshire stopped disclosing the company's earnings after 1994. ↩